Summary

- The US Federal Reserve (Fed) in July raised interest rates by a quarter-percentage point to a range between 5.25 to 5.50%. At the end of July, the benchmark 2-year and 10-year US Treasury (UST) yields were at 4.88% and 3.96%, down 2.1 basis points (bps) and up 12.2 bps, respectively, compared to end-June.

- The central banks of South Korea, Malaysia and Indonesia left their policy rates unchanged during the month. Price pressures moderated further in June.

- We see downward pressure on UST yields increasing as markets progressively price in the Fed’s rate hike cycle peaking. We retain our preference for Indonesian government bonds. As for currencies, we believe that greater support for the renminbi from Chinese policymakers should remove a near-term headwind for currencies in the region. We have a favourable view of the South Korean won and the Thai baht against such a backdrop.

- Asian credits returned +0.27% in July, as credit spreads tightened by 4 bps. Asian high-grade (HG) credit registered gains of 0.43%, while Asian high-yield (HY) credit retreated 0.66%.

- We expect macro and corporate credit fundamentals across Asia ex-China to stay resilient although slower economic growth looms over the horizon. Asian banking systems remain strong, with its stable deposit base, robust capitalisation and strong pre-provision profitability providing buffers against moderately higher credit costs ahead. However, given the slightly weaker macro backdrop and uncertainties, coupled with geopolitical tensions and the Fed’s policy path, the valuation of Asia HG credit looks slightly stretched compared to both historical levels and developed market spreads.

Asian rates and FX

Market review

The Fed raises rates by 25 bps in July

USTs started July on a weak footing as hawkish Federal Open Market Committee (FOMC) minutes and resilient US job market data increased expectations of another rate hike in the latter part of the year. However, the markets quickly dialled back expectations of a November hike following the release of June US inflation prints as headline and core numbers were both below expectations. The Fed raised interest rates by a quarter-percentage point to a range between 5.25 to 5.50%, with Chair Jerome Powell declaring that further increases would be contingent on inflation and activity data moderating in line with official forecasts. In Europe, the European Central Bank (ECB) raised its key interest rate in equal measure but signalled that it may soon pause, with President Christine Lagarde acknowledging deterioration in the Eurozone’s economic outlook. Towards the month-end, the Bank of Japan (BOJ) took what markets read as another step towards normalising monetary policy; the central bank relaxed its yield curve control (YCC) policy, under which it manages the benchmark 10-year Japanese government bond yield, prompting a jump in global yields. At the end of July, the benchmark 2-year and 10-year UST yields were at 4.88% and 3.96%, down 2.1 bps and up 12.2 bps, respectively, compared to end-June.

Chart 1: Markit iBoxx Asian Local Bond Index (ALBI)

| For the month ending 31 July 2023 | For the year ending 31 July 2023 | |

|

|

Source: Markit iBoxx Asian Local Currency Bond Indices, Bloomberg, 31 July 2023.

Central banks in South Korea, Malaysia and Indonesia leave policy rates unchanged

Bank Negara Malaysia left the overnight policy rate unchanged at 3.0%, stating that its monetary policy stance continues to be “slightly accommodative” and that the central bank “continues to see limited risks of future financial imbalances”. The Bank of Korea (BOK) left the door open for one more hike, with Governor Rhee Chang-yong declaring no change to the 3.75% terminal rate consensus among Monetary Policy Committee members. Over in Indonesia, the central bank extended its pause for the sixth consecutive month, keeping the benchmark interest rate at 5.75%. To spur bank lending, Bank Indonesia (BI) announced that targeted banks can lower their reserve requirement ratios by as much as 4%. Overall, the central bank reiterated that its focus remains on the stability of the Indonesian rupiah. It also left its growth forecast for the year unchanged at 4.5–5.3%.

Price pressures moderate further in June

A slower increase in food prices was a key factor that drove headline consumer price Index (CPI) readings lower in June. Consumer prices in Malaysia rose 2.4% year-on-year (YoY) in June, down from 2.8% in May. The moderation was prompted largely by lower price increases in food, restaurants and hotels. Similarly, core inflation climbed at a slower pace in June, rising 3.1% (from 3.5%). In Thailand, overall inflation eased to 0.23% YoY in June, undershooting the Bank of Thailand’s inflation target range of 1–3%, due in part to a slower rise in food prices and a high base. The core measure, which excludes fuel and food prices, similarly eased, printing 1.32% in June from 1.55% in May. Following the release of the CPI data, Thailand’s Commerce Ministry revised down its forecasts. It now expects overall CPI to gain 1–2% this year, down from 1.7–2.7% predicted previously. Singapore’s headline CPI moderated to 4.5% YoY in June from 5.1% in May on the back of a drop in private transport inflation along with the lower core inflation. Meanwhile, a significant easing in food inflation prompted Indonesia’s overall inflation to moderate to 3.52% in June. Elsewhere, headline CPI inflation in the Philippines eased for the fifth consecutive month in June, owing to slower increases in food prices and a faster decline in transport costs.

China’s Politburo pledges new economic support measures; Pan Gongsheng becomes new PBOC governor

Towards the end of the month, China’s Politburo acknowledged “new difficulties and challenges” for the Chinese economy, such as the lack of underlying demand, operational difficulties of certain companies and systemic risks in key industries all overlaying a complex external environment. For this reason, countercyclical support measures will be unveiled to support growth. Policymakers vowed to “elevate stable employment to a strategic goal”, boost consumption and defuse risk in local government debt. In addition, they pledged fresh support for the Big Tech sector and signalled stronger stimulus measures to aid the country’s troubled property sector. This prompted a significant rally in the renminbi and Chinese risk assets. Separately, Pan Gongsheng formally replaced Yi Gang as People’s Bank of China (PBOC) governor—a move that most market participants took as a signal that the government is prioritising policy continuity.

Market outlook

Prefer Indonesian bonds

The Fed’s current monetary policy tightening cycle is seen coming to—if not already at—a close, with fresh signs that pay and price pressures in the US are retreating. We see downward pressure on UST yields increasing as the markets progressively price in the rate hike cycle peaking. We retain our preference for Indonesian government bonds; the government has indicated that it will reduce bond supply this year amid healthy cash balances and budget surpluses. In addition, inflation is likely to moderate further, and BI has seemingly ended its hiking cycle.

South Korean won and Thai baht preferred

China’s recent Politburo meeting saw top leadership acknowledging issues that investors are most concerned with. Policymakers’ willingness to provide greater support could help stabilise the Chinese economy hereon, and the central bank has begun to support the renminbi, removing a near-term headwind for currencies in the region. We have a favourable view of the South Korean won and the Thai baht against such a backdrop. Demand for the won is likely to be supported by indications that a turnaround in the chip cycle is underway. Meanwhile, expectations towards the tech cycle improving, higher tourism revenue and relatively low oil prices amid a moderation in global economic activity are seen improving Thailand’s current account.

Asian credits

Market review

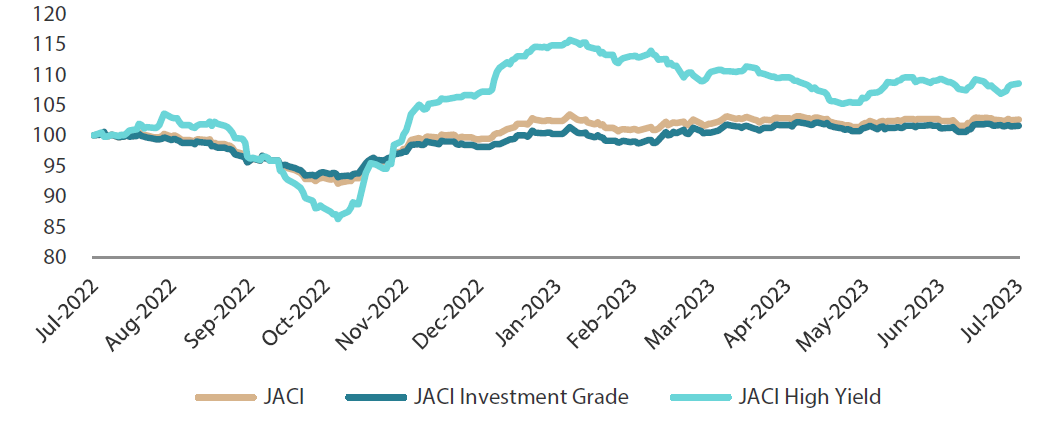

Asian credits register positive returns in July as credit spreads tighten

Asian credits returned +0.27% in July, as credit spreads tightened by 4 bps. Asian HG credit outperformed its HY counterpart, registering gains of 0.43% as spreads narrowed by about 8 bps. Asian HY credit retreated 0.66%, with spreads widening by 69 bps, owing largely to weakness in Chinese property credits.

Asian credit spreads had a firm start to July. However, sluggish China property sales numbers—together with news of a potential debt restructuring for yet another Chinese state-backed property developer—swiftly dampened sentiment, prompting a sudden reversal in spreads. Investor risk appetite remained subdued as data continued to point to a faltering Chinese recovery. Notably, although second-quarter GDP growth surged to 6.30% on a YoY basis— helped by a favourable comparison with 2022—the Chinese economy expanded by just 0.80% on a quarter-on-quarter basis, less than half the quarterly pace of 2.20% seen in the first three months of the year. HG credit spreads subsequently traded somewhat firmer, supported partly by favourable rhetoric from the Chinese government following Premier Li Qiang’s meeting with top technology firms. In contrast, HY credit spreads continued to widen, as concerns about the repayment ability of a handful of Chinese property companies weighed heavily on the property sector. Towards the end of the month, the Politburo finally acknowledged issues that investors are most concerned with, noting that the economy faces “new difficulties and challenges” and countercyclical support measures will therefore be unveiled to support growth. As policymakers signalled stronger stimulus measures to cushion downside risks for the economy and to aid the troubled property sector, Chinese risk assets rallied. Overall, spreads of all major country segments—save for China—tightened in July, with the strong performance of the Macau gaming sector helped by Standard & Poor’s rating upgrades of Las Vegas Sands and its subsidiary, Sands China.

UST yields moved higher in early July, as hawkish FOMC minutes and resilient US job market data increased expectations of another hike in November. That said, the markets quickly dialled back expectations of this following the release of June US inflation prints that undershot expectations. Towards the end of July, three major central banks made important moves. The Fed raised interest rates by 25 bps, with Chair Powell declaring that the FOMC will take a data-dependent approach on future hikes. The ECB raised its key interest rate in equal measure but signalled it may soon pause, whereas the BOJ decided to widen its YCC policy band to 100 bps from 50 bps. The BOJ move was broadly unexpected and prompted global yields to move higher. At the end of July, the benchmark 10-year UST yield was at 3.96%, up 12.2 bps compared to end-June.

Primary market quiet in July

Supply remained light in July, with issuers raising a total of just USD 5.76 billion in the primary market. The HG space saw eight new issues amounting to USD 4.70 billion, including the USD 1.0 billion issue from Korea Electric Power. Meanwhile, the HY space had four new issues amounting to USD 1.06 billion in the month.

Chart 2: JP Morgan Asia Credit Index (JACI)

Index rebased to 100 on 31 July 2022

Note: Returns in USD. Past performance is not necessarily indicative of future performance.

Source: Bloomberg, 31 July 2023.

Market outlook

Valuations slightly stretched but Asia macro and corporate credit fundamentals offer a sufficient buffer

China’s economic recovery momentum is softening. However, policy easing expectations are increasing across fiscal, monetary and property fronts—particularly after the supportive tone delivered by the July Politburo meeting. Therefore we expect policymakers to roll out more aggressive measures if signs of a cliff-like drop-off in sentiment and activity intensify. Macro and corporate credit fundamentals across Asia ex-China are expected to stay resilient despite slower economic growth in 2H 2023 and 1H 2024 as the effects of past monetary policy tightening begin to weigh and pent-up demand for services fade. Lower earnings growth and incrementally higher funding costs mean a slight weakening in leverage and interest coverage ratios for non-financial corporates in aggregate, but we believe that there is adequate ratings buffer for most, especially the HG corporates. Asian banking systems remain strong, with a stable deposit base, robust capitalisation and strong pre-provision profitability providing buffers against moderately higher credit costs ahead.

Given the slightly weaker macro backdrop and uncertainties ahead, including geopolitical tensions and Fed’s policy path, the valuation of Asia investment grade credit looks slightly stretched versus both historical levels as well as developed market spreads. As such, we take a more cautious view towards risk in the near-term.

Any reference to a particular security is purely for illustrative purpose only and does not constitute a recommendation to buy, sell or hold any security. Nor should it be relied upon as financial advice in any way.