The devil is in the details

Mainland China’s economy is in bad shape. Elevated youth unemployment is contributing to flagging domestic consumption, while households see the bulk of their savings, predominantly invested in real estate, dwindle as property prices spiral downwards. Dismal corporate earnings in the post-COVID years—caused by a tepid macro recovery and ongoing trade disputes with the US and Europe—have put local stock markets on the backfoot. Furthermore, the indiscriminate buying of financial derivatives, termed “snowballs” by retail investors, have exacerbated the downturn in equities.

It therefore came as no surprise that investors saw the raft of stimuli unveiled by the PBOC late in September as a much-needed reprieve from the litany of problems plaguing the country. Most major indices, such as the CSI 300, as well as names in the commodities space, rallied strongly. This is the most coordinated policy package announced by the authorities since the start of the economic downturn in Mainland China. This, along with the start of the Fed’s monetary policy easing, represents key fundamental changes. However, as the old saying goes, the devil is in the details.

A more apparent approach

In an opaque system where every little action is intensely scrutinised, the first thing we noticed was the manner that the official announcement was made. Gone are the days of trying to decipher tersely worded statements, which left much room for interpretation. This time, the top brass—PBOC Governor Pan Gongsheng, National Financial Regulatory Administration Minister Li Yunze and China Securities Regulatory Commission Chairman Wu Qing—jointly held a press conference for the foreign and local media.

This rare occurrence, in our view, signals a greater willingness by the authorities to be open and transparent regarding such policy shifts. The fact that the briefing was held at 9am China Standard Time rather than the typical 10am start also adds to our conviction that the authorities are serious about supporting growth, stabilising housing and stock prices, cushioning banks from further financial distress and arresting the deflationary spiral. Two days later, at a monthly meeting of top party officials, the Politburo, Chinese President Xi Jinping reiterated all the above and vowed to spare no effort to stem the decline in property prices, buttress household income growth, boost capital markets and alleviate prevalent youth joblessness. This was the first time a September Politburo meeting was devoted to the topic of the economy and gives further credence to the urgency that party officials attach to solving problems that could potentially destabilise social order.

Right time, right place

We believe that China’s financial regulators chose to implement the measures following the Fed’s first interest rate cut in more than four years to minimise downward pressure on the Renminbi. The central authorities’ efforts to help provincial governments refinance so-called “hidden debt” accumulated in state-owned financing vehicles also paved the way for these initiatives as well as more potential fiscal stimulus in the days ahead. In our view, these sweeping measures are the authorities’ aim to shore up softening growth as the 5% national target set for 2024 looks increasingly elusive. Prolonged weakness in the labour market has also hit a boiling point, necessitating crucial policy support to avoid social unrest.

Real estate reprieve

In the property sector, both existing mortgage and second home downpayment rates were cut. The PBOC chief also reiterated support for a Renminbi (RMB) 300 billion (USD 47 billion) relending facility. This facility, formed in May, is designed to boost the number of government-subsidised housing developments through the purchase of “reasonably-priced” commercial homes that have been completed. Real estate, a key driver of the economy, has been beset by developer defaults, unfinished projects and a glut in inventories, which have sent home values plunging. We believe long-standing key issues in the sector, such as falling rental yields and pricing with developers, have yet to be addressed. This means that attempts at reducing surplus inventory may not be resolved in the near term.

Liquidity boost and a shot in the arm for the stock market

Several moves have been made to inject more liquidity in the economy, such as lowering the reserve requirement ratio for banks by 50 basis points (bps) and a 20 bps reduction in the seven-day reverse repo rates. These measures seem to dovetail neatly with changes to capital markets that give brokerages, insurance firms and mutual funds access to a RMB 500 billion swap facility to buy domestic shares. Additionally, plans are underway for a RMB 300 billion relending programme for listed companies and large stakeholders to conduct share buybacks. This is expected to improve investor confidence in the battered stock markets. We view this as a prudent move, given the success of similar “stock market rescue programmes” implemented in many other economies such as Taiwan.

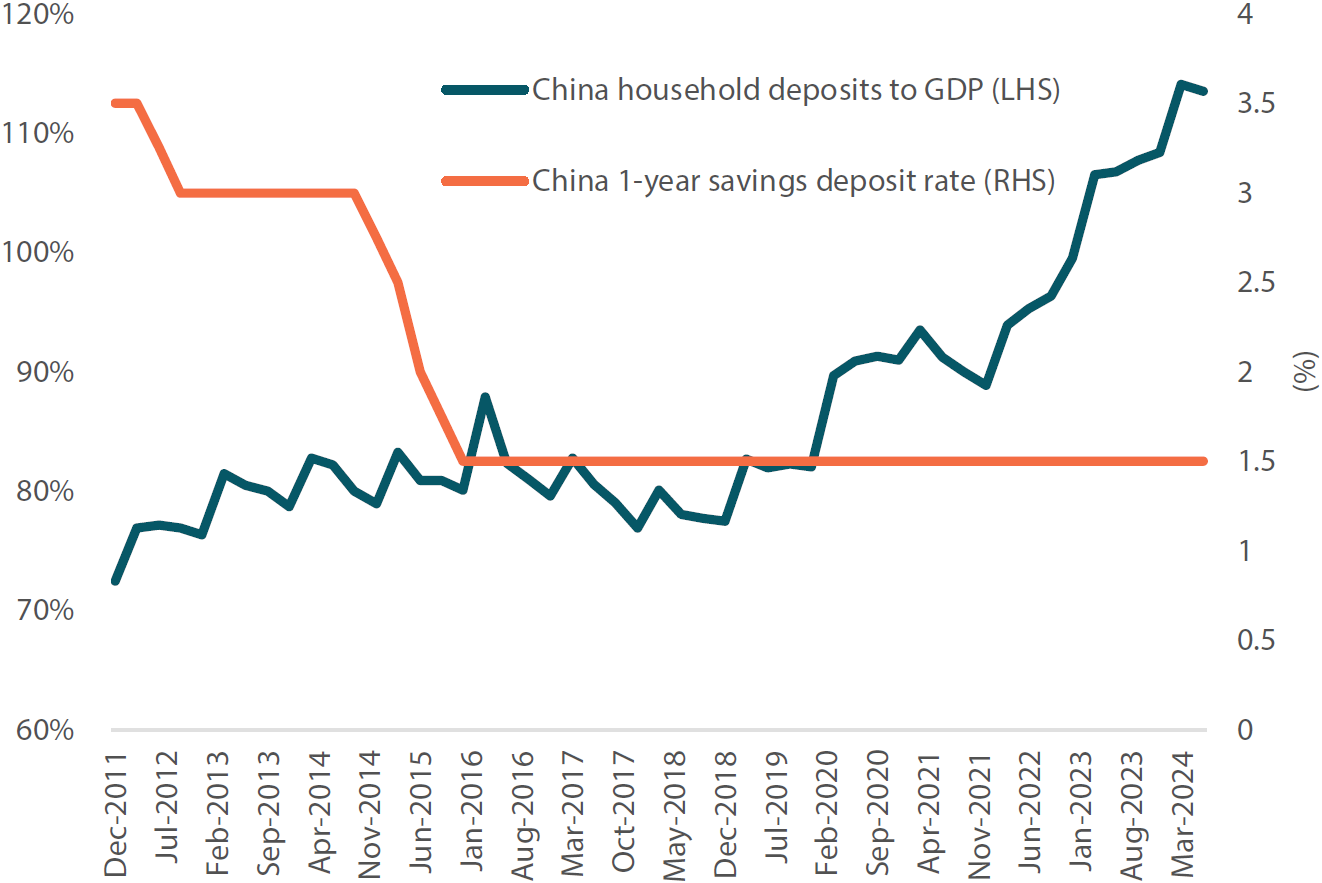

We believe these moves are positive for Chinese equities, and investors may consider companies with low price-to-book ratios that have the capacity to buy back shares. Furthermore, the initiatives are likely to attract the attention of Chinese investors, who have been focused on debt repayment or parking their money in deposits (Chart 1).

Chart 1: Household deposits to GDP versus 1-year savings interest rates

Source: China National Bureau of Statistics, PBOC, April 2024

Although these measures may have “no limits” according to PBOC Governor Pan, they cannot be classified as full quantitative easing. This is because the monetary authority is not directly intervening in the way the Fed has been doing for years, but merely providing the tools. Another caveat is that any funding from the central bank must be backed by collateral, meaning that only firms with solid balance sheets and healthy assets will be in a better position to leverage the additional resource. All the China A-shares we assess meet this threshold. Moreover, for the stock market rally to continue, we believe further meaningful fiscal spending has to be unleashed.

More fiscal firepower required

Looking past the cheer generated by the stimulus, we think the Chinese central government has its work cut out, with broader structural issues to tackle. Providing support for a rapidly aging population is a concern, as net outflows from the pension system exceed inflows. This is a consequence of the one-child policy finally scrapped in 2015. The government, however, has enacted reforms to raise the statutory retirement age and create a buffer as it attempts to backfill the shortfall.

Meanwhile, the youth unemployment rate continues to rise as fresh cohorts of university graduates enter the job market each year. The authorities’ drive to transition the economy up the value chain from low-end to high-tech, advanced manufacturing and services has not yet fully absorbed the excess labour capacity. This, in turn, depresses wages and weighs on domestic consumption, another key pillar of the economy. In response, Chinese cities have expanded subsidies, introduced in March this year, on a range of home appliances and electronics until the end of 2024. Additionally, the government will distribute one-off cash handouts to disadvantaged groups. President’s Xi’s pledge to focus on employment for affected groups, including fresh graduates and migrant workers, may also hint at further initiatives to address this pressing concern in society.

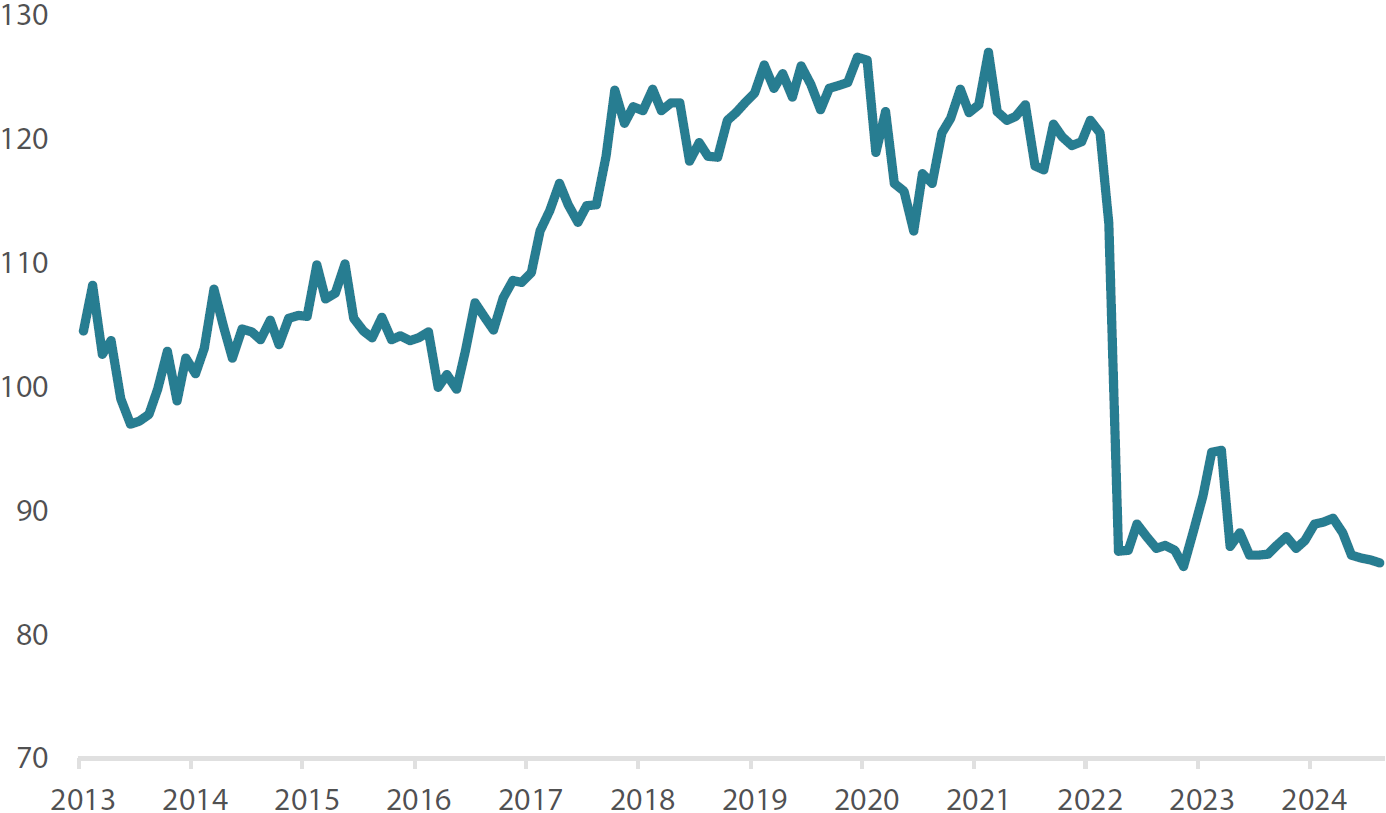

From our observation, the elephant in the room seems to be a lack of consumer confidence (Chart 2). It is hard to feel optimistic about the future when job security is tenuous, salaries remain stagnant and as investors see the value of their real estate and equity holdings depreciate by the day. To be sure, we believe many Chinese households still have ample savings set aside for rainy days and there is no major liquidity shortfall in capital markets. But perhaps what is really needed is for the authorities to deploy the proverbial “big guns” and fulfil their promises to push out more fiscal policies. Such a move could address this crisis of confidence, improve risk appetite and reflate the economy.

Chart 2: China consumer confidence levels

Source: China National Bureau of Statistics, PBOC, April 2024