Summary

- Asian stocks turned in solid gains in December, buoyed by optimism about a vaccine-led global economic rebound, fresh US fiscal stimulus and robust economic data from China. The MSCI AC Asia ex Japan Index rose 6.8% in US dollar (USD) terms over the month.

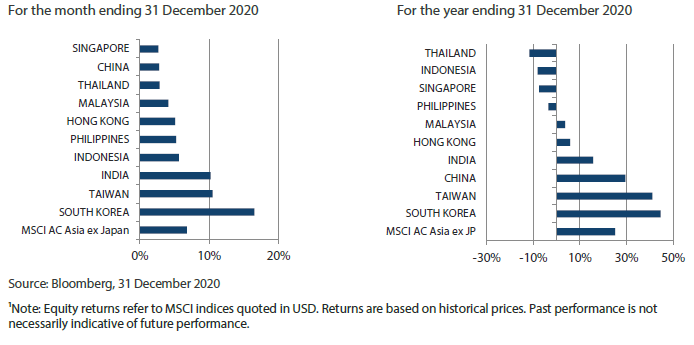

- South Korea, Taiwan and India were the best performers in December. Investors bet on a swifter economic recovery in South Korea and India, while Taiwan was boosted by strength in its semiconductor stocks.

- China lagged its regional peers, dragged by technology shares after Beijing launched an anti-trust probe into Jack Ma's Alibaba Group. There were also signs of tension between the US and China, with Washington set to add dozens of Chinese companies to a trade blacklist.

- We maintain our focus on the structural positive changes brought about by the pandemic. We continue to see opportunities to gain exposure to quality companies which would enjoy more sustainable returns as a result of these changes. These include domestic-focused companies in structural growth areas of software, automation, healthcare and insurance.

Market review

Regional stocks lifted by hopes of a vaccine-led global economic rebound

Asian stocks ended 2020 strongly after turning in solid gains in December. During the month, market sentiment continued to be buoyed by optimism about a vaccine-led global economic rebound, as several countries around the world started to roll out mass vaccination against the coronavirus. Fresh US fiscal stimulus and robust economic data from China also cheered investors ahead of the year-end holiday period.

For the month, the MSCI AC Asia ex Japan Index surged 6.8% in US dollar (USD) terms, outperforming the MSCI AC World Index, which rose 4.2%. Within the region, South Korea, Taiwan and India were the best performers in USD terms (as measured by the MSCI indices), while Singapore, China and Thailand were the laggards.

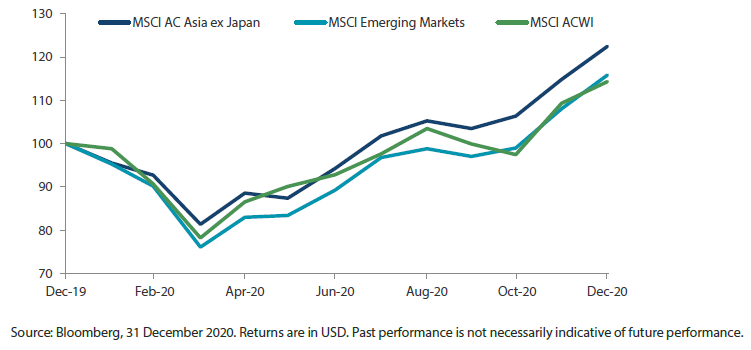

Chart 1: 1-year market performance of MSCI AC Asia ex Japan versus Emerging Markets versus All Country World Index

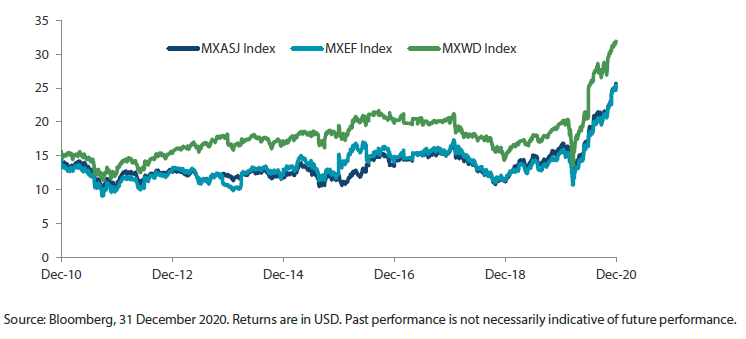

Chart 2: MSCI AC Asia ex Japan versus Emerging Markets versus All Country World Index price-to-earnings

South Korea and Taiwan outperform

In South Korea, stocks jumped 16.6% in USD terms in December, driven by the strong performance of index heavyweight Samsung Electronics, as investors bet on a swifter economic recovery in the country. South Korea's December exports expanded at their fastest pace in 26 months, owing to strong global demand for chips, display sets and mobile devices.

Likewise, Taiwanese stocks performed well for the month, rising 10.5% in USD terms, led by giant chipmaker Taiwan Semiconductor Manufacturing Company and other semiconductor names. Taiwan's manufacturing purchasing managers index (PMI) rose for the sixth straight month in December, recording its strongest reading since January 2011.

India tracks the regional upswing

In India, stocks turned in USD gains of 10.2% in December, as signs of economic recovery and positive developments on the COVID-19 vaccine front continued to support the market. India's manufacturing PMI rose slightly to 56.4 in December from November's 56.3. During the month, Moody's raised India's economic growth forecast for 2021 from 8.1% to 8.6%.

Singapore, Thailand and China lag

In the ASEAN region, all equity markets turned in positive returns in December. Indonesia, the Philippines and Malaysia saw decent USD gains of 5.6%, 5.2% and 4.1%, respectively, for the month; on the other hand, Thailand and Singapore delivered dreary USD returns of 2.9% and 2.7%, respectively. In Indonesia, the government forecast that GDP will grow between 4.4% and 6.1% in 2021, largely driven by an expected recovery in consumer spending after vaccines become widely available and fiscal stimulus packages take effect. Elsewhere, Singapore's economy, according to preliminary data, shrank by a record 5.8% in 2020 and 3.8% in the fourth quarter from a year earlier, surpassing consensus expectations.

In China, stocks lagged their regional peers and returned 2.8% in USD terms in December; gains were tempered by technology (tech) shares after Beijing launched an anti-trust probe into Jack Ma's Alibaba Group. There were also signs of tension between the US and China throughout the month, with Washington set to add dozens of Chinese companies to a trade blacklist. In Hong Kong, stocks tracked the regional upswing and delivered USD gains of 5.1% for the month.

Chart 3: MSCI AC Asia ex Japan Index1

Market outlook

Global economic recovery looks set to continue apace

As we turn the page on a turbulent 2020, with vaccines being rolled out as we speak, there are many positives to look forward to in 2021. Notwithstanding the persistently high number of COVID-19 cases and lockdown in parts of the West, the global economic recovery looks set to continue apace, although it could be some time before the large output gap is closed. Where we are focused on are the structural positive changes as a result of the pandemic. An area of change we have observed is the reforms initiated during the heights of the pandemic, as Asia saw the crisis as an opportunity to push through changes, especially in countries such as China and India. We have also been sensitive to permanent changes in consumer and corporate behaviour post the pandemic, and we continue to see good opportunities in quality companies which would enjoy more sustainable returns as a result of these changes. These include domestic-focused companies in structural growth areas of software, automation, healthcare and insurance.

China maintains commitment to transform its economy

For all of its troubles with Donald Trump's US, China has not neglected its commitment to transform its economy. That for the first time ever China does not have an explicit economic growth target in its 14th Five-Year Plan is significant in its shift from "quantity to quality". The much discussed "dual circulation" strategy at its core is about China's endeavour to remain open to the world (international circulation), while engineering a shift from infrastructure-led growth to innovation- and consumption-led growth domestically (domestic circulation). In the shorter term, the prudence of the regime to tighten ahead of any over-exuberance bodes well for the country's longer-term sustainable growth. Accordingly, we continue to favour areas of improving domestic demand, localisation and strategic industry development.

Focusing on private sector banks, digital services and logistics in India

Similar to China, India is also determined not to waste a crisis as it makes structural improvements to its economy. Indian Prime Minister Narendra Modi's government has proactively pushed through labour and agriculture reforms during the pandemic, all of which could be transformative if executed well. Labour reforms have relaxed onerous restrictions on lay-offs, fixed-term employment and unions, thereby boosting efficiency and encouraging investments in labour-intensive sectors. Agriculture is one such sector which would also benefit from the recent passage of reforms announced in May via a much-needed investment in the supply chain, which makes it more efficient. We continue to focus on sub-sectors benefiting from trends such as market consolidation, formalisation and companies that reduce the friction of doing business, namely private sector banks, digital services and logistics.

South Korea and Taiwan at the forefront of innovation and technology

At the forefront of innovation and technology, many South Korean and Taiwanese companies are poised to be big beneficiaries of the permanent change in consumer and corporate behaviour. Whether it is in the increasing demand for technology, healthcare, industrial automation or clean energy, many South Korean and Taiwanese companies have positioned themselves to be critical parts of the supply chain in these structural areas.

Selective in ASEAN

Parts of ASEAN have been some of the hardest hit during the pandemic. However, with mobility restrictions easing and vaccines being rolled out, these are also countries poised to bounce back the hardest as "normalisation" gets underway, although it might take time. While we expect strong upwards revisions in terms of earnings and economic activities, we continue to be selective and focus on areas where there could be sustainability of returns post recovery, such as electric vehicle materials and high-quality banks, both of which we have found in Indonesia.

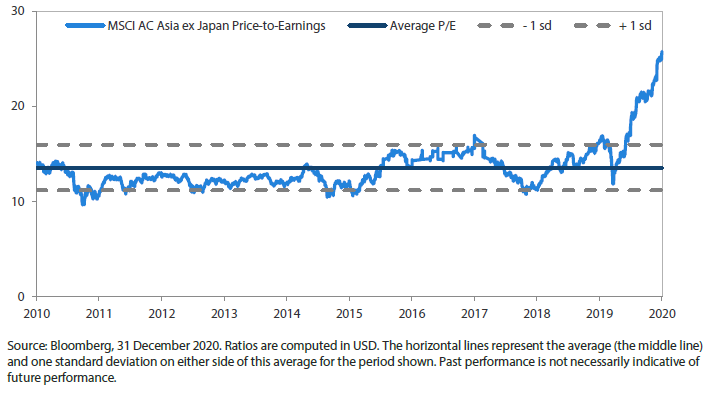

Chart 4: MSCI AC Asia ex Japan price-to-earnings

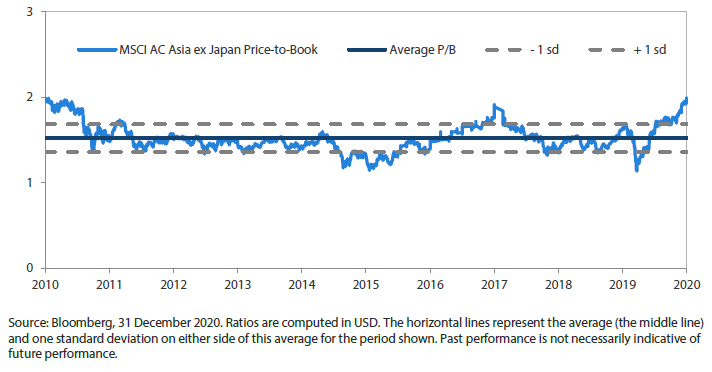

Chart 5: MSCI AC Asia ex Japan price-to-book